How Deregulation Could Accelerate U.S. Infrastructure

And What It Means for Industrials & Materials

For decades, building almost anything in America has meant wrestling with long environmental reviews, overlapping permits, and a slow-moving bureaucracy. A bridge or highway could spend more time in the planning pipeline than under construction. In 2025, that dynamic is shifting. A sweeping deregulatory push out of Washington is aiming to cut through red tape, speed up approvals, and unlock a new wave of energy and infrastructure projects.

If that shift sticks, it could have important implications for industrial and materials companies that supply the equipment, steel, concrete, and services behind big builds.

A Second-Term Deregulatory Blitz

When President Trump returned to the White House in January 2025, his administration wasted little time reviving its earlier deregulatory agenda. On his first day back in office, he signed an executive order branded “Unleashing American Energy,” directing agencies to roll back rules seen as obstacles to infrastructure and energy development.¹ The Council on Environmental Quality (CEQ) was pushed to rescind and rewrite National Environmental Policy Act (NEPA) regulations to accelerate environmental review and permitting.¹

The Environmental Protection Agency then added fuel to the fire. In March 2025, EPA chief Lee Zeldin announced what he called “the greatest and most consequential day of deregulation in U.S. history,” outlining 31 actions to reconsider or repeal rules on power plants, drilling, vehicles, and industrial emissions.² The stated goal: lower compliance costs, cheaper energy, and a more competitive manufacturing base.²

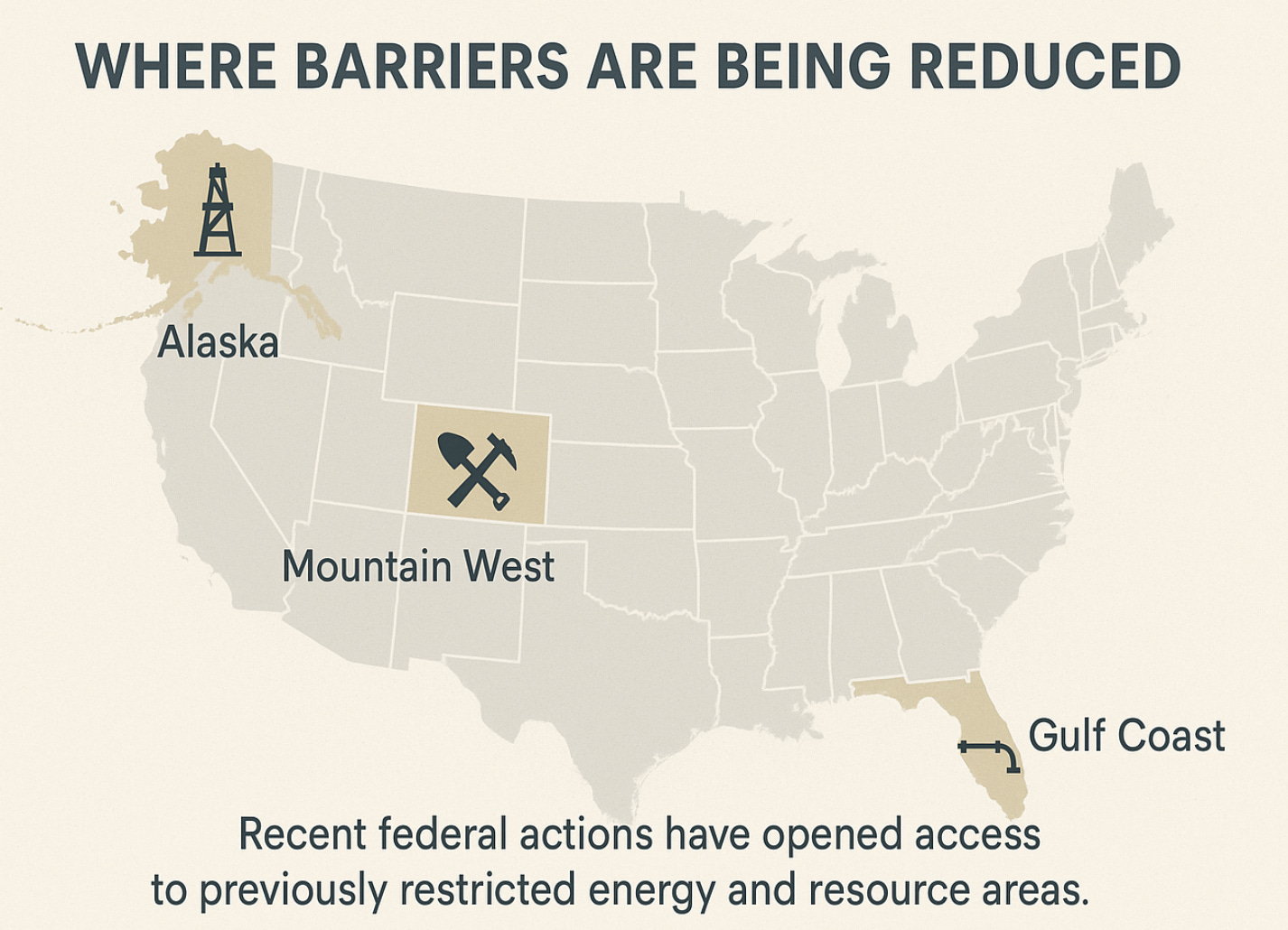

The energy patch has seen some of the most dramatic moves. In October 2025, the Interior Department opened 1.56 million acres of the Arctic National Wildlife Refuge to oil and gas leasing, reversing a prior ban and advancing other projects in Alaska’s National Petroleum Reserve and the Ambler Road mining corridor.³ Interior Secretary Doug Burgum framed the decisions as unlocking Alaska’s resource potential and strengthening U.S. energy independence.³

For companies tied to drilling, mining, and large-scale construction, these decisions effectively widen the opportunity set. More green lights in resource-rich regions mean more potential demand for pipes, steel, machinery, and on-the-ground services.

Cutting Red Tape in Infrastructure Permitting

Some of the most consequential changes are happening in the less visible world of federal permitting. Here, the administration is not just loosening individual rules—it is rewriting the process itself.

In June 2025, Transportation Secretary Sean Duffy unveiled the first comprehensive update to the Department of Transportation’s NEPA procedures in roughly forty years.⁴ He argued that the old system empowered “unelected Washington bureaucrats” to delay or block critical projects, and promised a leaner playbook that would “slash red tape” and fast-track delivery of roads, bridges, and other infrastructure.⁴

The new USDOT rules impose page limits and hard deadlines on environmental documents, expand “categorical exclusions” for low-impact projects, and encourage agencies to avoid duplicative analysis.⁴ The intent is straightforward: a highway lane addition, rail upgrade, or airport expansion that once languished for years in environmental review should now move to groundbreaking much faster.

Other agencies are adjusting in parallel. The Fiscal Responsibility Act of 2023 set statutory deadlines for environmental impact statements and assessments, and departments such as the Army Corps of Engineers and the Department of Energy have been aligning their procedures with those timelines.¹ Reviews are increasingly happening concurrently across agencies rather than sequentially, reducing the cumulative delay.¹

Early indicators suggest the reforms are beginning to matter on the ground. A long-delayed road improvement near Yuma Proving Ground in Arizona wrapped up on schedule in early 2025, with officials pointing to smoother federal coordination and a clearer permitting path as part of the reason.⁵ The National Association of Counties has also flagged significant implications for local governments, noting that everything from roadwork to broadband projects could move faster under the updated NEPA guidance.¹

If these procedural changes continue to take hold, America’s infrastructure “to-do list” could start clearing more quickly than in the past, with knock-on effects for sectors tied to construction and logistics.

Industrials & Materials: Where the Opportunities Are

Deregulation is ultimately about real projects, not just policy headlines. If more highways, pipelines, transmission lines, and industrial facilities move from blueprint to shovel-ready, demand naturally flows toward the companies that make and move heavy stuff.

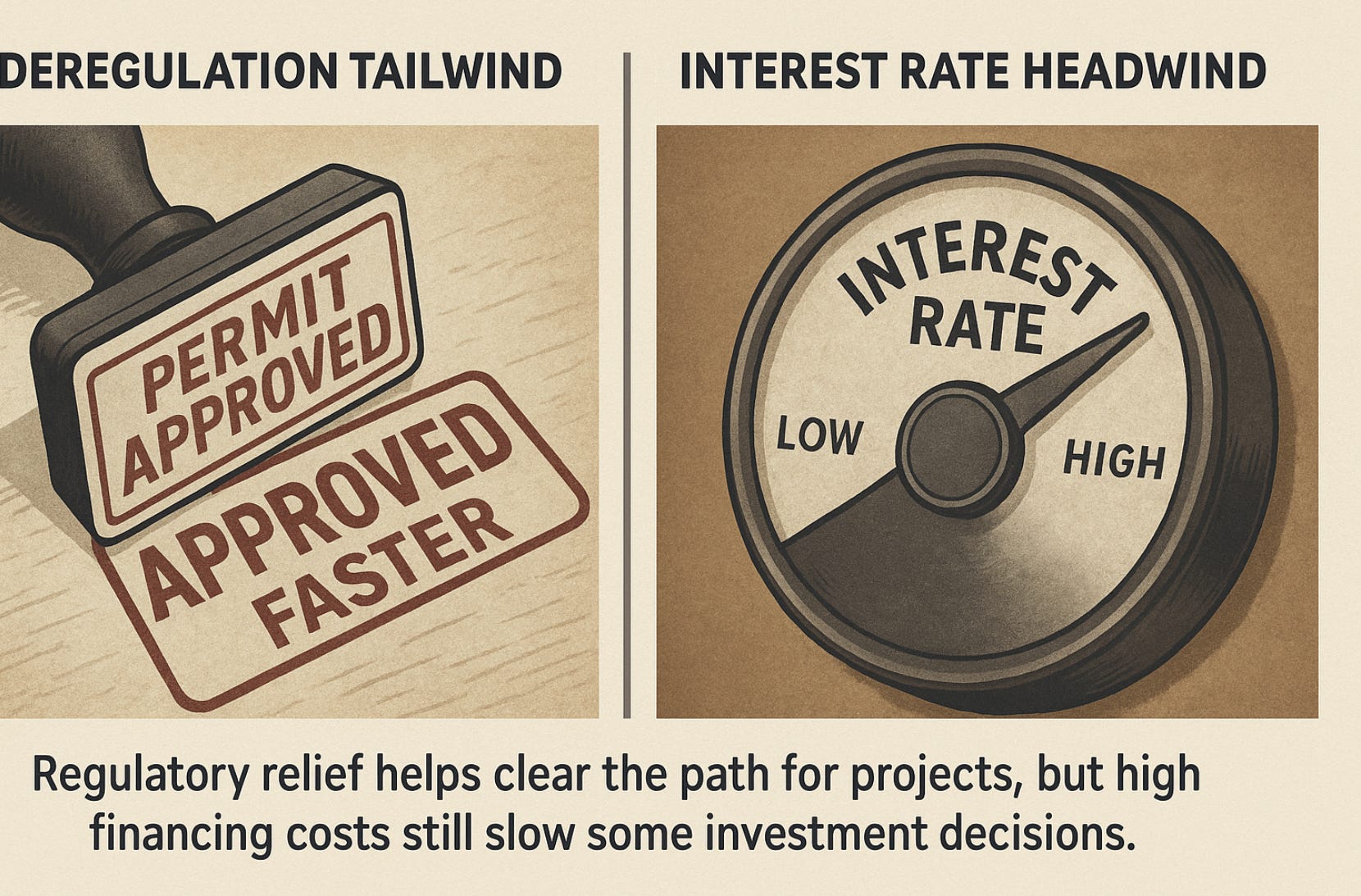

Caterpillar, often seen as a bellwether for global construction, is one of the most obvious names tied to this theme. In early 2025, the company’s finance chief acknowledged that if deregulation successfully boosts U.S. growth and infrastructure activity, “it would benefit Caterpillar.”⁶ The logic is simple: faster approvals mean more projects breaking ground, which in turn means more orders for excavators, loaders, and power systems.

Caterpillar has already benefited from the 2021 federal infrastructure law, but that tailwind is no longer accelerating the way it did initially.⁶ At the same time, high interest rates have made some customers more cautious about buying new equipment, even as the regulatory environment becomes more permissive.⁶ In other words, policy is pulling one way while monetary conditions pull the other.

On the materials side, the connection is even more direct. Martin Marietta Materials, one of the largest U.S. suppliers of aggregates and cement, has posted strong results and raised its outlook on the back of “sustained infrastructure demand.”⁷ That demand has been driven by ongoing government-funded highway and construction programs, as well as a growing “AI-era” build-out of data centers and related infrastructure.⁷ If deregulation leads to an even larger pipeline of public and private projects, companies like Martin Marietta could see an extended cycle of elevated volumes.

Steel is another obvious beneficiary. Nucor, America’s largest steelmaker, has expanded capacity with an eye on infrastructure spending and favorable policy shifts. Analysts have highlighted how deregulation and supportive trade measures can improve profitability for steel tied to pipelines, grid upgrades, and large industrial projects.⁸

The firms best positioned to benefit are likely those that can respond quickly to new demand: regional contractors, engineering and construction companies, equipment rental providers, and suppliers with flexible production. Companies that already invested heavily to meet stricter standards may also enjoy a structural cost advantage if operating rules become less burdensome for everyone else.

Risks, Constraints, and the Bigger Picture

Even in a friendlier regulatory climate, investors need to remain realistic. Policy tailwinds can create opportunity, but they do not eliminate risk.

First, deregulation is not guaranteed to be permanent. Many of the 2025 rollbacks face legal challenges from environmental groups and state governments. Court decisions could delay or even reverse some changes, particularly in environmentally sensitive areas such as the Arctic and other protected lands.³ A future administration might also restore tighter standards, reintroducing uncertainty for long-lived projects.

Second, financing conditions still matter. The Federal Reserve’s tight stance has raised borrowing costs, and high interest rates have arguably become a bigger brake on new construction than environmental paperwork in some cases.⁶ Companies may have permission to build but still decide to hold back if capital is expensive or if they are worried about the broader economic outlook.

Finally, there is the environmental and social dimension. Opening more land to drilling or pushing projects through faster can generate backlash from local communities and environmental groups. Over time, reputational damage, remediation costs, or new restrictions can all affect returns. Companies that manage to navigate the new, looser rulebook without ignoring long-term environmental risks may be better positioned than those that simply race to build at any cost.

Conclusion

Deregulation has emerged as a defining economic story of 2025. By cutting back on red tape and compressing permitting timelines, Washington is attempting to swap years of bureaucratic delay for a more streamlined “yes or no” process on infrastructure and energy projects. The early signs—from completed roadwork to upbeat commentary by materials and equipment suppliers—suggest that the pipeline is starting to move.⁵⁷

For investors, the theme can be framed as a “build-out trade”: industrials, materials, and related service providers that benefit when the country builds more, faster. But it is not a one-way bet. Interest rates, court challenges, political turnover, and environmental concerns all have the potential to reshape the story.

The takeaway is not that deregulation guarantees a boom, but that it materially improves the odds that shovel-ready ideas actually make it into the ground. In a world where timelines matter, that alone can be a powerful catalyst for industrial America.

Footnotes

National Association of Counties, “Federal Agencies Release NEPA Guidance Following White House Executive Order 14154,” August 2025.

U.S. Environmental Protection Agency, “EPA Launches Biggest Deregulatory Action in U.S. History,” news release, March 12, 2025.

“Trump Administration Opens Arctic Refuge to Oil Drilling,” The Guardian, October 23, 2025.

U.S. Department of Transportation, “U.S. Transportation Secretary Sean P. Duffy Unveils Sweeping Updates to NEPA at USDOT to Fast Track Roads, Bridges, & Other Key Infrastructure,” press release, June 30, 2025.

“Imperial Dam Road Improvement Project Wraps Up in Early 2025,” Defense Visual Information Distribution Service (DVIDS).

“Caterpillar Warns of Sales Drop in 2025 on Weak Equipment Demand,” Reuters, January 30, 2025.

“Martin Marietta’s Quarterly Profit Rises on Sustained Infrastructure Demand,” Reuters, November 4, 2025.

“Nucor Corporation: Gaining Strength from Deregulation and Tariffs,” Seeking Alpha.

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.